In the days leading up to Adam Neumann’s ouster as CEO of WeWork in September, theories around WeWork’s corporate governance were in full swing. Neumann’s move to cash out $700 million of his holdings compounded a series of absurd decisions, including a reorganization earlier in the year where the company paid its own CEO $5.9 million for the “We” trademark, granted Neumann loans to buy properties WeWork would then rent, and hired several of his relatives. While this saga demonstrated a serious lack of accountability and an unsustainable governance structure, it was also reflective of an increasingly common notion in organization theory: key-person risk.

According to The Economist, key-person risk occurs when “an individual’s presence, absence, or behaviour disproportionately affects a firm’s value.” The loss of a key person could prove to be a firm’s biggest liability, affecting everything from company finances to its image or investor confidence. In WeWork’s case, the company’s S-1 acknowledged that if Neumann were absent, it could have a material adverse effect on the business. It went so far as to state that Neumann was “critical to our operations” and “key to setting our vision, strategic direction, and execution priorities.” In November, WeWork laid off almost 20% of its global workforce.

At WeWork, key-person risk did not originate solely from the founder’s charisma or strategic vision. The governance structure permitted it; from the S-1:

From the day he co-founded WeWork, Adam has set the Company’s vision, strategic direction and execution priorities. Adam is a unique leader who had proven he can simultaneously wear the hats of visionary, operator and innovator, while thriving as a community and culture creator. Given his deep involvement in all aspects of the growth of our company, Adam’s personal dealings have evolved across a number of direct and indirect transactions and relationships with the Company. […]

Adam controls a majority of the Company’s voting power, principally as a result of his beneficiary ownership of our high-vote stock. Since our high-vote stock carries twenty votes per share, Adam will have the ability to control the outcome of matters submitted to the Company’s stockholders for approval, including the election of the Company’s directors. As a founder-led company, we believe that this voting structure aligns our interests in creating shareholder value.

WeWork’s multi-class stock structure, in conjunction with Neumann’s delusions of grandeur and his complex web of personal and professional dealings as CEO, were emblematic of key-person risk. Companies operating with such a practice concentrate outsize power to their founders and early employees under the assumption this ensures prioritization of long-term objectives. But it may also make management less accountable to shareholders. According to the CFA Institute, a dual-class structure may “reduce the oversight of public, unaffiliated shareholders who have the majority of the economic stake but a minority of votes,” but can vary in nature.

Alphabet and Omega

Take Google’s parent company Alphabet, whose co-founders Larry Page and Sergey Brin stepped down on December 3rd. On the news of their departure, Alphabet’s shares rose slightly. And yet, Page and Brin will continue to have effective control over the company, remaining on the board with a majority of voting shares.

The co-founders’ gradual (and well-documented) disappearance from operations at Alphabet has deterred any potential over-reliance on them as key executives. The same cannot be said of Google CEO Sundar Pichai, who is succeeding Page and Brin at the helm. Pichai will be simultaneously the company’s largest asset and liability:

- Whereas Pichai was previously head of the core search engine operations, he will begin overseeing new and emerging segments of the business, from driverless cars to AI and life extension technology. Since the core business accounts for 85% of the company’s sales, Pichai has over the past few years been more of a “key person” within Alphabet than either of its founders.

- A fundamental reworking of the culture could be in order following a series of internal protests at Google around claims of harassment, civic and labor rights, executive mismanagement, and a number of contentious hires. Most of the organizers of the Google Walkout have since resigned. Pichai’s handling of the crisis will set the tone.

- Looming antitrust investigations around Google’s ad business and YouTube’s financials will raise questions around the company’s anti-competitive practices. Pichai, who has already testified in Congress on issues ranging from data privacy to political bias, will undergo even greater scrutiny as CEO of the parent company.

It’s difficult to lump in Pichai with typical examples of key-person risk. He has been called “very cautious” by coworkers, known for his steady management style. But those qualities may also be characteristic of stagnation; from FT:

The new Alphabet chief is not without an idealistic streak. A committed globalist, he is deeply interested in technology’s potential to transform countries such as his native India. But taming the worker upheaval is a priority. Employees may have believed they have “signed up for a movement,” but the company is becoming a far more conventional place to work, one former Googler said. […]

Internally, Mr. Pichai is a known quantity and not expected to make significant changes. That could make him different from Mr. Nadella, who pushed Microsoft in a new direction.

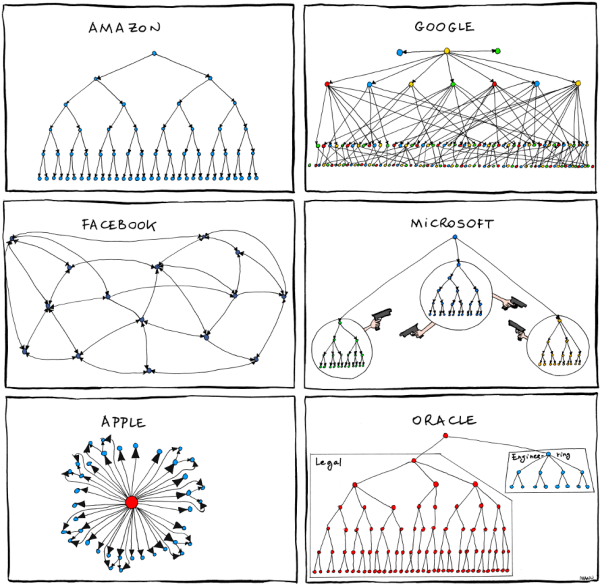

Pichai may nonetheless experience a situational type of key-person risk, being put in a position where he becomes indispensable to Alphabet irrespective of his performance. Manu Cornet, a software engineer at Google, famously illustrated the differing management styles at top tech companies in his 2011 comic “Org Charts” (cited by Satya Nadella in Hit Refresh as one of the drivers for changing the culture at Microsoft).

With Brin and Page exiting stage left, Alphabet’s organizational chart should be updated to reflect a more archaic structure, short of a rigid Amazonian hierarchy. In addition to the core business of search, mobile, hardware, and cloud services, Pichai’s focus will extend to a slew of more obscure and long-term projects, including DeepMind AI, Calico (health and wellness), Sidewalk Labs for urban infrastructure, and more. Control over all these entities will make Pichai an indispensable presence, for better or worse.

Achievement Unlocked

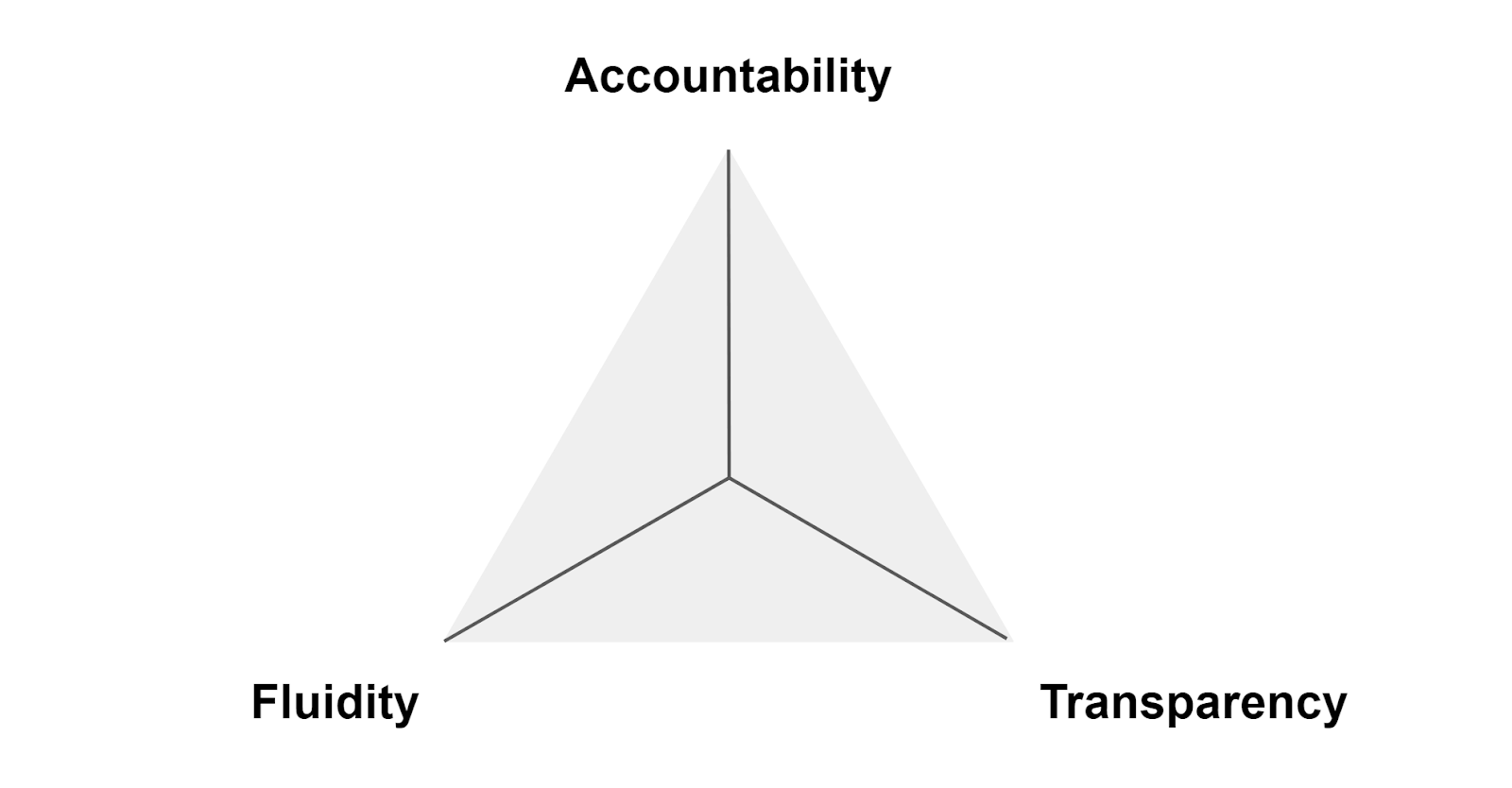

Taking the above into account, I propose the following framework for identifying and managing the variants of key-person risk.

To avoid dependency risk, organizations need to create a governance structure that is simultaneously accountable, fluid, and transparent:

- Accountability: Organizations often fall prey to key-person risk by proactively enabling senior leadership and failing to implement a proper mechanism for checks and balances. Carlos Ghosh, the former chairman of the global alliance between Nissan, Renault, and Mitsubishi is one such example. Ghosn, who is currently on trial for financial misconduct and leveraging corporate resources for personal gain, was considered an irreplaceable maestro without whom the empire would crumble. Other structures are also responsible for unaccountable leaders; for instance, dual-class share structure can erode corporate accountability in certain cases by watering down shareholders’ voting power.

- Fluidity: The most effectively run organizations are prone to a more detrimental type of key-person risk: executive lock-in. If organizational culture is fluid, it creates a structure where managers are easier to remove when they start making poor decisions. Jack Ma, who stepped down as Chairman of Alibaba in September, understood this; he contends that the right system is one with a robust leadership system “that can create, can make, and can discover, can train a lot of leaders.” Daniel Zhang, Ma’s successor as executive chairman, argues that the best succession plans are those that ensure a leader will fight for the vision, mission, and values of a company.

- Transparency: When leaders are not transparent with their board, their employees, or the public at large, they create developmental hurdles. The concentration of knowledge to a single person inhibits organizations from adapting to industry trends. If a business is opaque or financially complex (i.e. SoftBank), a key-person could have tacit knowledge that makes them vital to operations. Jony Ive’s departure from Apple demonstrates the inverse scenario: the loss of institutional knowledge.

Let’s take each one in turn.

Accountability

The first is when an individual with a lot of influence (i.e. control over a majority of voting rights) fails to spread responsibility, lacks accountability, and appoints feckless subordinates. Facebook finds itself in this predicament, with Mark Zuckerberg controlling nearly 60% of voting rights and unwilling to make changes to the firm’s governance structure.

In its Oversight Board Charter released in September, the social media giant set forth some parameters for its board composition, the main purpose of which would be to “protect free expression by making principled, independent decisions about important pieces of content and by issuing policy advisory opinions on Facebook’s content policies.” Ideally, this would raise transparency and clarity around the reasoning for decisions relating to content; from the Charter:

Members must not have actual or perceived conflicts of interest that could compromise their independent judgment and decision-making. Members must have demonstrated experience at deliberating thoughtfully and as an open-minded contributor on a team; be skilled at making and explaining decisions based on a set of policies or standards; and have familiarity with matters relating to digital content and governance, including free expression, civic discourse, safety, privacy and technology.

And yet, none of this oversight is more democratic than before. The charter represents a firewall that shields the company’s executives from scrutiny. The board’s responsibility will instead be to issue recommendations around policy that Facebook can choose to support, but only “to the extent that requests are technically and operationally feasible and consistent with a reasonable allocation of Facebook’s resources.” It’s largely toothless and does not intend to make the firm more accountable.

Fluidity

A second variety of key-person risk occurs when a leader excels in their role. While this type of leadership can improve performance, the dependency risk that results may prove detrimental to both the succession process and long-term sustainability of a business. But this can be avoided if the governance structure is fluid and adaptable. In Microsoft’s Momentum, I argued that Satya Nadella’s tenure represented a shift in both culture and priorities:

Culture is what allowed Microsoft to become a dominant player, cementing Windows as the only clear option for enterprise IT managers. But the same exact assumptions that allowed Microsoft to scale – that it would (with its unmatched resources) inevitably develop a superior solution, or continue leveraging its Windows dominance into the end of days – later constrained its ability to make a directional shift when required. By looking beyond their golden goose and betting instead on a cloud-based future, Nadella precipitated Microsoft’s revival.

The sagas resulting from this dependency risk have made good fodder for screenwriters. One example of this is HBO’s Succession, a dark comedy (with tones of King Lear) that follows an obstinate patriarch, Logan Roy, the CEO and founder of an international media conglomerate, Waystar Royco. Facing declining health, Logan contemplates the future of his business and ultimately decides not to step down, thwarting several family members in the process.

Succession is reminiscent of the winding path to power at real-life media businesses, and the role of managing key-person risk in boosting confidence. Sumner Redstone, the media mogul who was formerly executive chairman of CBS and Viacom, oversaw the break-up of the two companies in 2006, declaring that the age of the diversified media conglomerate had come to an end. Over the past few years, his daughter Shari (now the chairwoman at ViacomCBS) has attempted to remerge the businesses on several occasions, but received significant pushback. The merger was completed on December 4th.

Transparency

The third – and most nuanced – variant of risk affects companies with a governance structure so complex that a singular perspective is required to maintain confidence. While WeWork tried to frame itself in this lens, I believe that their unaccountable executive places them squarely in the first category. Instead, it is WeWork’s main investor, Masayoshi Son of SoftBank (colloquially known as Masa), who fits this description.

Over the past few years, SoftBank has been characterized by a series of poor judgments. The Vision Fund raised $45 billion from Saudi Arabia in spite of global scrutiny around their human rights record, and several of its high-profile bets – WeWork, Uber, Slack – have seen mounting losses. Masa himself has been accused of recklessness on conference calls, alternating from charming one moment to enraged or demanding the next; from FT:

The technological evangelism of Mr Son divides opinion. “He is a visionary,” says Dan Baker, an analyst at Morningstar who rates the company a buy. “He is extremely bullish and rarely mentions negatives. Investors are wary of what is not being talked about.”

These include “complexity, opacity, and leverage,” according to Chris Hoare of New Street Research. Even compiling a sum-of-the-parts valuation – a simple exercise for most conglomerates – is tricky for SoftBank. But the discount between the impressive value of the group’s investments and its lowly Tokyo-listed shares is over 60 per cent, according to FT analysis of S&P Global data.

The chasm is hardly flattering for Mr Son. It implies his investment skills – or a perceived lack of them – have a negative impact equivalent to $148bn. The boss of a quoted private equity company could be fired for a discount as big as this.

Masa also invests in founders who are risk-seeking and erratic (much like himself), which can sometimes be an asset: his first bet of $20 million in Alibaba’s Jack Ma paid off. But this does not necessarily make for a good governance structure. In a recent CNBC interview about the pervasive effect of SoftBank on the technology space, Masa claimed the company is “just a small startup,” albeit one with 100bn at their disposal.

Concerns have been raised around SoftBank’s lack of transparency. Masa rarely addresses negatives, such as the gap between the value of SoftBank’s investments and the price of its shares – which, alongside years of poor returns, have soured investor confidence around the company’s $100bn Vision Fund (and its successors). In spite of all this, investors would likely panic if Masa were to resign. As with unequal voting rights, financial complexity can entrench leaders in an organization. In the case of SoftBank, it has provided Masa with significant job security.