One of the policies in contention at the G7 summit in France last month had little to do with climate change, finance, or disease eradication. In a renewed effort to placate the U.S. (and to avoid potential tariffs), French President Emmanuel Macron announced that a digital tax on revenues put into effect earlier this year could be deducted by companies that pay, but only once a new international deal is ratified.

The Digital Services Tax (DST), passed by the French Senate in July, would approve a 3% levy on revenue coming from digital services earned in France by firms with over €25m in national revenue and over €750m worldwide. With these parameters, the tax would apply to around 30 major companies (mostly U.S.-based). This has earned a sharp rebuke from Internet giants like Amazon, Google, and Facebook, which accuse the French government of targeting foreign technology companies. The U.S. Trade Representative, Robert Lighthizer, added that he would investigate whether the law “is discriminatory or unreasonable and burdens or restricts United States commerce.”

What’s interesting here is the attempt by these firms to frame the bill as a departure from the current global tax regime. Nicholas Bramble, the trade policy counsel for Google, said the law threatens the processes laid out in the OECD, undermining the multilateral momentum around the modernization of tax rules for multinational corporations. Moreover, he claims that “efforts by one country to unilaterally change the rules on how profits are allocated among countries can generate new barriers to trade and hamper economic growth.”

And yet, the multilateral OECD process has not been an effective conduit for international tax reform in some time. Austria, Belgium, Britain, Italy, and Spain are all contemplating a digital services tax in light of the EU’s recent failure to reach an agreement. Amazon, Google, and others are most likely not advocating multilateral action to preserve the integrity of the international tax regime. Instead, perhaps they hope that any proposal which is so widely accepted is bound to be watered down and relatively harmless.

Bramble makes a fair argument with his claim that the bill would tax just a handful of e-commerce or Internet businesses. With economic sectors like healthcare and manufacturing becoming increasingly digitized, it is not clear that the DST is a catchall solution that bridges the divide between where profits are taxed and where the firms’ digital activity is carried out. In an excerpt from EY’s Global Tax Policy and Controversy Briefing, Rob Thomas and Chris Sanger clearly lay out the confines of the digital taxation issue:

The current debate is not about tax avoidance or the existence of stateless income. It is, rather, about the division of tax rights among countries who consider that their citizens contribute to the profits made by some digitally focused companies, even if they do so via unconventional means.

At issue, then, is how to craft a measure that not only addresses this value creation problem but also does not raise concerns over the perceived discrimination of a handful of digital companies. But that did not seem to be the French government’s objective. The DST, which politicians and media outlets in France had dubbed the ‘GAFA Tax’ (an acronym for the targeted firms: Google, Apple, Facebook, and Amazon), would have primarily applied to U.S.-based companies. If anything, this law reflects the view that the global tax regime crafted in the early 20th century has failed to predict the radical transformation of transnational corporations over the past century.

A Discriminatory Measure

In retaliation to the announcement of the bill, the Trump administration threatened a tax on French wine, calling the measure a comprehensive attempt at “[targeting] innovative U.S. technology firms that provide services in distinct sectors of the economy.” In its criticisms, the USTR decried the DST’s retroactive application from the start of 2019, which it deemed unfair, and listed three reasons why the tax is unreasonable:

- Extraterritoriality

- Taxing revenue not income

- It targets a handful of tech companies

Take each one in turn. National laws are often crafted with extraterritoriality in mind, that is, laws that apply to individuals or firms outside of a nation’s borders. While it has in the past been associated with the cross-border activity of digital companies (e.g. the GDPR), extraterritoriality can also apply to issues like crime, sanctions, and diplomatic immunity. But the Internet complicates things. Online activities that are legal in one country can be illegal in another. Governments across the EU may be starting to regret taking a ‘light touch’ in allowing the Internet’s unfettered growth to persist early on, and attempt to create a set of parameters around measuring digital activity in two or more jurisdictions.

Also at the heart of the debate around digital taxation is France’s decision to tax revenue (turnover) rather than income. In the case of the DST, a 3% levy would apply to gross revenue from activities in which users “play a role” in creating value. These could include the following:

- Placing ads on a digital interface which are aimed at its users

- Making available a digital interface allowing users to find and interact with each other, and thereby facilitating a transfer of any underlying goods or services between them

- Transmission of user-generated data on these digital interfaces

Whereas some digital companies would be within the scope of the proposed DST, like online advertisers or platforms aimed at connecting users to trade goods or services, others could be excluded due to their limited scope in contributing to “value-creating” activities. This lack of clarity extends to online marketplaces with little or no user-to-user selling, yet where there may be a lot of user-generated content. SaaS firms which offer data analytics and other cloud services could fit somewhere in between.

Thirdly, the USTR claims that the French tax is unfair since “its purpose is to penalize particular technology companies for their commercial success.” There is some truth to this. The measure is targeted by nature and would hit around 30 tech companies, most of which are U.S.-based. France highlights a ‘dual injustice’ and argues that SMEs pay an average tax rate around 14 points higher than large digital companies, and that French citizens’ personal data are used to create value for these enterprises. The Finance Minister, Bruno Le Maire, has also stated that the DST would affect only a single French company, raising concerns around the benchmarks set around digital taxation.

Digital Value Creation

Whereas some characteristics of digital firms are clear, there are many blurred lines. Traditional sectors are increasingly exhibiting similar attributes as digital firms, a trend visible in areas like academia, healthcare, and agriculture. As the OECD works towards a consensus on the ideal digital services tax by 2020, it will have to consider the distinction between digital and digitized businesses: the former provides digital services, whereas the latter is operationally reliant on digital tools for its survival.

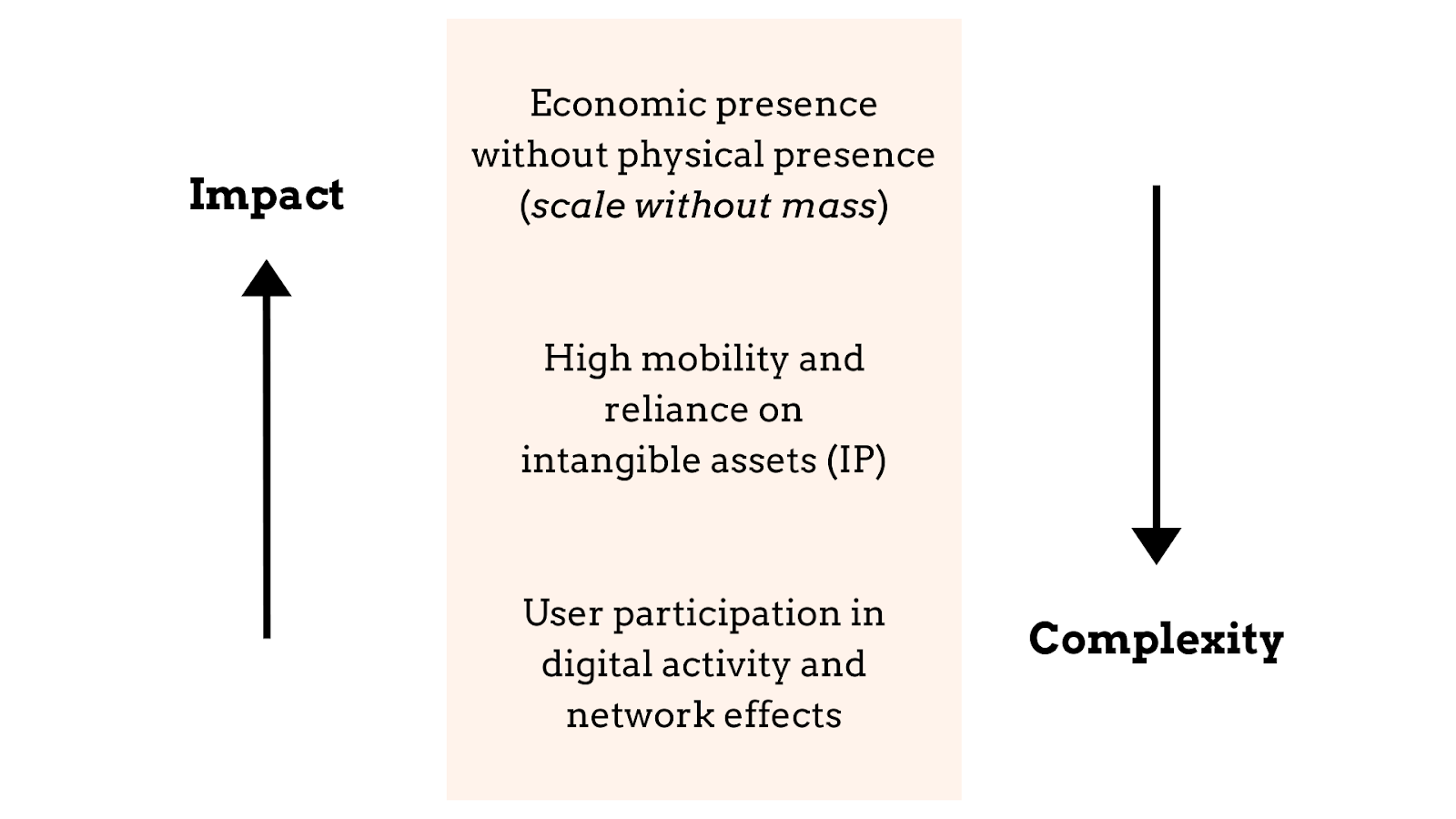

A complete diagnosis of the value creation mismatch would point to a few factors. Companies today can provide a wide array of digital services in areas where they are not physically present, a practice the Commission dubs “scale without mass.” The reproduction of this phenomenon has lowered the number of jurisdictions where the international tax regime can assert taxing rights on the profits of multinational companies. Moreover, digital businesses have typically been characterized by their reliance on intangible assets like IP, indicating a higher level of mobility.

The third feature of digital companies is a data-driven business model that is predicated on user participation, characterized by network effects and user-generated content. But this is difficult to measure, especially in a framework which distinguishes purely digital companies from those (in manufacturing, healthcare, etc.) which are caught up in, and adapting to, an increasingly digital economy. The debate is therefore around whether and how this creates value, according to Freshfields Bruckhaus Deringer, a law firm:

[…] notably, countries are divided as to whether this third limb contributes to value creation. Some countries argue that it does, on the basis that users provide digital companies with data that can be monetized (either by using it to improve services or selling it to third parties) and content that can be used to attract and retain other users. In addition, these countries argue, network effects mean that by participating via a digital platform, users increase the value of the platform to advertisers and potential users alike. The idea of user-generated value underpins the Commission’s proposals. Other countries, however, disagree: user-generated data and content is equivalent to sourcing inputs from independent third parties, and thus under normal taxation principles should not be seen as value-creating.

But are “normal taxation principles” relevant to digital firms? An effective framework for digital taxation would need to overturn these principles and redefine what activities are value-creating. With the increasing digitization of our economic processes, the conventional notions of service providers and cross-border activity are no longer applicable.

The result is a digital value-creation framework that looks like this:

Ultimately, scale without mass is the most impactful feature of a highly digital business model, given that these companies can have significant effects on the economy of multiple jurisdictions without any physical presence whatsoever. But it is also the least complex of the three limbs of digital companies, which explains why France and others have been using it as the benchmark for measuring lost revenue. Moving forward, it will be necessary for unilateral and multilateral solutions alike to consider all value-creating elements of digital businesses.

To address the scale without mass issue, it is imperative that the third limb (user participation) is also included in the framework and deemed a value-creating activity. There are two reasons for this. First, it will allow individual countries and institutions to craft laws that will be more accurate and less discriminatory in targeting a specific kind of digital business. One obvious example of this is social networks, which have a much greater level of involvement from users than cloud computing or data archiving. Second, some businesses would not exist today if it were not for user-generated content and network effects.

Tax Nationalism

The whole debate around the DST is suffused with economic nationalism. In a rush to ensure that large digital companies pay their fair share of taxes, the French government is encouraging other member states to impose similar unilateral measures to the detriment of an OECD-wide solution. But previous institutional attempts to create a digital taxation framework have led to an impasse, and there is decreasing confidence in the OECD to devise a multilateral measure that is unanimously approved. Countries do not want to waste time in capturing the spoils of a digital economy.

On the other hand, American tax nationalism is not just presidential bluster – it is codified in federal laws. According to Section 891 of the Internal Revenue Code (IRC), the U.S. President has the right to double the income tax rates on foreign nationals and firms that are operating domestically when “under the laws of any foreign country, citizens or corporations of the United States are being subjected to discriminatory or extraterritorial taxes.” The USTR has threatened to do just that if the DST provision were to be implemented, under the guise of preventing “significant double taxation.”

Another problem relates to jurisdictions and the risks involved with unilateral measures. Gary Clyde Hufbauer, an economist at the Peterson Institute for International Economics, argues that the DST is misguided largely because of this; from PIIE:

The French digital tax is ill-considered firstly because it contravenes the “permanent establishment” principle for dividing the profits of a multinational company between two or more taxing jurisdictions. Under current tax treaties, the existence of a permanent establishment — some sort of physical presence — is the threshold for including a portion of corporate profits in the domestic tax base. Digital firms, including U.S. tech giants, purvey their websites globally with no physical presence in most countries.

Hufbauer also cites Section 301 of the Trade Act of 1974, allowing the U.S. President to deem certain measures “unreasonable, discriminatory, or unjustifiable,” open an investigation, and if affirmative, subsequently place trade restrictions on exports on, say, French wine. Although the heyday of Section 301 use was in the Reagan era (in which current USTR Robert Lighthizer served), rules around trade in services, IP rights protection, anti-competitiveness practices, or foreign trade policy had not yet been codified. Its contemporary use would not be in line with formal WTO settlement dispute procedures, and indicates a reversion to the nationalism and aggressive unilateralism largely characteristic of the 1980s.

Hufbauer continues:

The claim is often made that the Internet calls for a new threshold for dividing the corporate tax base. But until a new threshold is agreed between countries, national self-help measures, like the proposed French tax, will result in double taxation and discourage the spread of digital commerce, one of the strongest forces now lifting the global economy.

While I agree that a multilateral solution and consensus around the definition of digital benchmarks are essential to divvying up the corporate tax base, resorting to antiquated laws is not the solution. The Trade Act and the IRC were respectively released in 1974 and 1986, both prior to the formation of the WTO and the notion of a digital enterprise. If OECD processes were to stall and nations are left to their own devices (not an unlikely scenario), the tax framework depicted above could, at the very least, represent a starting point in the process of measuring digital value-creation.

Can I simply say what a reduction to find somebody who actually is aware of what theyre talking about on the internet. You undoubtedly know how to deliver an issue to mild and make it important. More people have to read this and perceive this facet of the story. I cant consider youre not more common because you definitely have the gift.

LikeLike