The most successful players in the digital payments space are those that design their core products in such a way that recognizes the different functions of money and facilitate their execution. One of these is Stripe, a fintech firm that processes mobile and online payments on behalf of companies like Airbnb, Twilio, and GitHub. Early on, its business consisted of providing an API to e-commerce firms by linking them to card networks and banks. But Stripe has grown, and the company now offers a wider array of services including fraud protection, credit cards, and incorporation services.

Patrick Collison, Stripe’s CEO who co-founded the company with his brother John in 2010, argues that working with card networks has been the aim from the start, saying it was “always clear there was no viable independent strategy.” Last month, Stripe raised a $250m round at a valuation of $35bn, coming on the heels of many new product updates and international expansion. Stripe’s continued diversification, alongside aggressive growth and intelligent branding, are making the payments startup more competitive.

A hackable medium

In finance, the concept of money is frequently defined in terms of the three functions it serves. As a medium of exchange, money can facilitate transactions – and without it, bartering would be the primary method of exchanging goods and services. As a store of value, money can be stored for a given period of time and remain valuable in exchange at a later date. And finally, as a unit of account, money acts as a common measure of value for goods and services, recording debts, or making calculations.

Money and the notion of exchange through payments have both evolved drastically since their inception from barter to metal coins and banknotes, or bank accounts to e-wallets. The digital payments market is forecast to reach 7.64 billion USD by 2024, recording a CAGR of 13.7% in the period from 2019-2024. But in areas like payment security, concerns persist. Although the shift to EMV chip cards in the U.S. has led to a decrease in counterfeit card fraud, criminals are creating synthetic identities to apply for and receive EMV credit cards to defraud merchants and banks.

One answer could be contactless payments, which are set to emerge as a preferred option across the industry. Contactless has a higher rate of adoption in countries like Canada, the UK, Australia, and South Korea – with the latter having the highest rate of contactless cards in force at around 96% in 2016. The US, meanwhile, had less than 3.5% of such cards in force that same year, reflecting cost efficiencies on behalf of banks. With popular mobile tap systems like Apple Pay catching on (it controls 10% of the global smartphone market and half in the US), the mobile contactless user base has grown considerably, from 20 to 144 million in the 2015-17 time period.

Contactless payments operate thanks to short-range wireless technology like radio frequency identification (RFID) or near-field communication (NFC) to secure payments with a compatible point of sale terminal. Although such transactions are appealing due to their ease-of-use and speed (at around 1/10th of the time of a conventional electronic transaction), adoption has also proven slower in some countries due to security concerns. Consumers are worried that cybercriminals could compromise their card data; from Investopedia:

There have been stories in the media about criminals skimming card data using smartphones to read tap cards in consumers’ wallets. The range at which a card can be read is very short and, even if the criminal is close enough to grab data and do a transaction, he cannot create a copy of the card. This is not true of magnetic strip cards. That said, the chip and pin card is still the most secure, as they can’t be duplicated and they require data (your pin) that is not contained anywhere on the card.

Merchants and credit card companies are increasingly being considered liable for fraudulent activity if they lack chip technology. Fintech companies are taking note. In June, Stripe announced its Terminal product, consisting of “a set of SDKs, APIs, and pre-certified card readers,” extending the company’s payment system to allow for in-person payments. According to Devesh Senapati, a Product Manager at Stripe, the Terminal’s pre-certified card readers have built-in protection from counterfeit fraud for in-person transactions, and support both chip cards and contactless payments.

Another factor contributing to the digital payments boom has been an explosion in the Internet penetration rate, from 35% global penetration in 2013 to 57% this year. This is making optical QR codes, on which many e-wallet apps are increasingly reliant, a more appealing option. In China, where WeChat Pay and Alipay are the dominant players, QR codes are omnipresent in retail and convenience stores, restaurants, and even movie theaters. Implementing QR codes is a cheaper alternative to NFC technology, and its inherent security has made it the driving force in digital payments across the country, allowing consumers and sellers to interact without point-of-sale terminals.

Defining monetary value

When discussing money, how to define its function as a store of value? Is it somewhere to put one’s life savings (transferring purchasing power from the present to the future), and if so, what are the parameters? To help crystallize monetary value in the context of Stripe, let’s take a look at two examples and long-term initiatives within the company: digital currencies and access to money.

New money

There has been a longstanding debate around whether cryptocurrency fulfills the core functions of money. Bitcoin, for instance, can be used as a medium of exchange, although the fluctuations in transaction confirmation times and fees could make it less useful as a method of payment. There is less of a consensus that cryptocurrencies are a store of value, given their volatility – while Bitcoin can be saved and exchanged at a later date, there has been disagreement over the immutability of its network. According to William Wu, a Wharton Student Fellow, Bitcoin also fails at being a unit of account since it does not indicate the real value of an item, acting instead as “an intermediary between the item and the fiat currency with which it is being exchanged.”

Although it ended its support of Bitcoin in 2018 (largely for the reasons listed above), Stripe has long been supportive of cryptocurrencies more broadly. John Collison, Stripe’s president and co-founder, expressed excitement for crypto’s potential at Recode’s Code Commerce conference in 2018, saying “if we want to offer easy APIs to pay out to long-tail countries, we think there could be a bunch of interesting ideas there.” For regions lacking well-functioning payment systems, Stripe sees significant potential in digital currencies as a medium of exchange. It also provided seed funding for a crypto network called Stellar early last year.

There have been some bumps along the way. On October 2nd, the Wall Street Journal reported on that Stripe (alongside PayPal, Visa, Mastercard, and many others) would back out of its membership in Libra, the cryptocurrency-based payments network created by Facebook. Critics and regulators alike have argued that Libra could be used for illicit purposes like money laundering, with Treasury Secretary Steven Mnuchin calling the project “a national security issue,” and the head of the Federal Reserve expressing similar reservations.

One of the primary reasons Stripe reconsidered its involvement in the Libra project was the heightened level of regulatory scrutiny, made clear in a letter from Sens. Brian Schatz (D-HI) and Sherrod Brown (D-OH). In it, the lawmakers argued that Facebook has failed to provide a plan for how it will avoid facilitating activities like terrorist financing, monetary policy intervention, or destabilizing the global financial system. They argue this will compound the issues currently faced by the social network; from the letter:

Facebook is currently struggling to tackle massive issues, such as privacy violations, disinformation, election interference, discrimination, and fraud, and it has not demonstrated an ability to bring those failures under control. You should be concerned that any weaknesses in Facebook’s risk management systems will become weaknesses in your systems that you may not be able to effectively mitigate. […] If you take this on, you can expect a high level of scrutiny from regulators not only on Libra-related payment activities, but on all payment activities.

The external pressures on Facebook itself were made clear in a series of tweets by David Marcus, who heads the Libra project:

Although there are regulatory hurdles around the deployment of Libra, it’s unclear whether the project’s members would have been committed with more lax regulation. Given Facebook’s record on user privacy and security, many partners are dubious that the social network could act entirely independently from its cryptocurrency project. In his testimony at the House Financial Services heading on Wednesday, Facebook CEO Mark Zuckerberg said that the company could even be forced to leave the Libra Association if U.S. regulators did not approve.

Stripe will not be waiting on lawmakers. In February, the payments company led a funding round for Rapyd, a “fintech as a service” startup which offers services ranging from funds collection to currency transfers and ID verification. Although Rapyd doesn’t currently offer support for crypto, CEO Arik Shtilman said they are looking into such services down the line – providing Stripe with a hedge against Facebook and potentially circumventing the regulatory pressures of such initiatives.

Financial inclusion and access

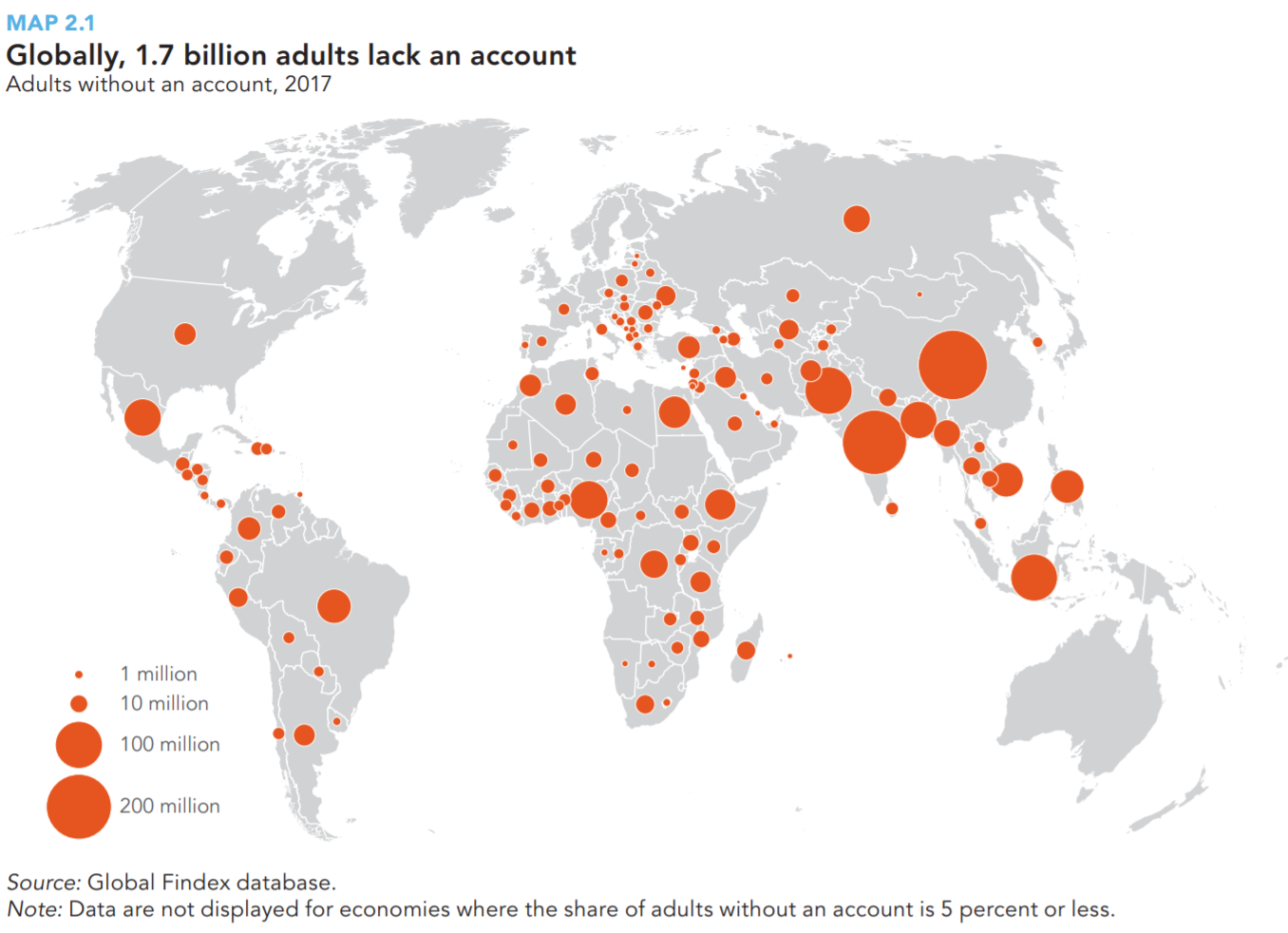

Any truly global payments network should also aim to enable financial inclusion. This notion refers to the process whereby vulnerable groups – or regions – are ensured access to financial products and services, according to the RBI, “at an affordable cost in a fair and transparent manner.” As of 2017, around 1.7 billion adults worldwide remain unbanked, according to the World Bank – that is, without an account tied to a financial institution or through a mobile money provider; from Global Findex:

Since many traditional payments systems never reach people in countries with underdeveloped banking systems, fintech firms have penetrated developing markets through a different medium. Although 90% of Bangladeshis do not have bank accounts, around 75% have access to mobile phones, providing most with the capacity to make digital payments. This has led to the rise of firms like bKash, a payments system that processes around 5 million daily transactions across Bangladesh. bKash, through which customers can open accounts that run on a fully encrypted platform, is facilitating digital payments nationwide.

One of Stripe’s main objectives is democratizing access to money. It recently launched Stripe Capital, a service to make instant loan offers to customers on its platform. Through this service, cash advances – which are a staple for competitors like PayPal and Square – are repaid out of future sales through Stripe’s payment platform, with the customer’s transaction activity acting as a basis for loan amounts and repayments. As with credit cards, the aim of Stripe Capital is to provide customers with “quick (next-day) access to funds to help both with daily liquidity as well as to invest in growth,” which could be of particular use in the developing world.

William Gaybrick, Stripe’s CFO, is eyeing Southeast Asia’s digital payments market. According to the South China Morning Post, the lack of dominant digital payment providers and low credit card penetration are key reasons for the push. Stripe’s continually expanding offering make the expansion a no-brainer, and its existing partnerships with WeChat Pay and Alipay have already unlocked a market accounting for half of total worldwide mobile wallet spending.

John Collison has long framed Stripe as a “[provider of] infrastructure for the Internet economy,” going beyond merely processing payments and adapting to the changing dynamics of the retail landscape by making smaller companies more competitive. But whether Stripe succeeds in the next wave of digital payments will depend on how its services leverage the core functions of money as a medium of exchange, store of value, and unit of account.