In his book Envisioning Real Utopias, the American sociologist Erik Olin Wright laid the foundations for a reconstruction of the core values for socio-economic progress. One of Wright’s central themes throughout the book is that capitalism can impose on democracy, countering Milton Friedman’s claim that capitalism is a “necessary, but not sufficient, condition for democracy.” Wright notes the following:

The key issue, then, is that the private decisions of owners of capitalist firms often have massive collective consequences both for the workers inside of the firm and for people not directly employed in the firm, and thus the exclusion of such decisions from public deliberation and control reduces democracy. A society in which there are meaningful forms of workers’ democratic control within firms and external democratic public control over firms is a more democratic society than one which lacks these institutional arrangements.

To counter the pernicious effects that capitalism can have on democracy, and the “massive collective consequences” that firms’ actions can have on their employees and the broader public, many companies have made it their mission to promote inclusion. This is especially true of finance. In an industry which has historically been controlled by a handful of institutions and banks, and not the general public, the lack of meaningful internal or external checks to corporate activity has proven detrimental to broader collective-democratic processes.

The Internet has changed some of this. One of the most significant steps towards this goal of inclusivity has been equity crowdfunding, in which an individual investor does not need to be a financial professional or require accreditation to participate in the market. As ordinary investors lack the full range of investment and financial services available to professionals, some firms have staked their claim on opening up markets to the general public.

But even unchecked, there are many challenges to the crowdfunding model and its inclusion of the average consumer. According to a Gallup poll from April last year, around 55% of Americans own stocks, down from 67% at its peak in June 2002. 2016 data from the Federal Reserve indicates that a much smaller share of families, 14%, are directly investing in individual stocks, versus market investment through retiring accounts like 401(k)s. Presence in the stock market itself is also not evenly distributed; NYU professor Edward Wolff found that over half of all households in the U.S. own shares either directly or indirectly, but the richest 10% of households controlled 84% of the total value of these stocks.

Market Manipulation

The above preamble helps to deconstruct this week’s decision by Robinhood, a financial services company, to restrict transactions for numerous securities.

Much of Robinhood’s decision-making seems to have stemmed from the recent spike in the share price of GameStop (GME), one of the world’s largest video game retailers. The market frenzy had been stoked up by users of r/wallstreetbets, a Reddit forum with over 7.4m followers. A few members on the forum pointed to the involvement of Ryan Cohen, the former CEO of Chewy, which PetSmart acquired in 2017. Cohen had begun to amass a large stake in GameStop last August, with the long-term goal of investing in its e-commerce operations. In November, Cohen’s stake in GameStop was valued at roughly $79 million.

It would be euphemistic to say that not everyone based their actions on the fundamentals. Many on Reddit lamented the high barriers to entry to participating in the market, and expressed a desire to stick it to Wall Street, alongside the investors and hedge funds that placed short sells on GME and other stocks; from The Economist:

The retailer had become a target of short-sellers, who borrow shares, sell them, and later buy them back, ideally at a cheaper price. It was a popular trade: the total value of short positions in GameStop was more than the company’s market capitalization in late January. Retail investors wanted the shorts to lose money.

And they did. Bullish retail traders were ginned up when the marketmakers who sold them their bets were forced to hedge against rising prices by buying shares. Short-sellers were also forced to buy shares after incurring losses worth several billion dollars. The wall-to-wall coverage of the stock has prompted yet more investors to pile in. GameStop was the single most traded stock in America on January 26th; volumes matched that in the five biggest tech giants combined. The share price more than doubled the next day. The masses are coming for other heavily shorted stocks too. Share prices for AMC, a chain of cinemas, and Nokia and Blackberry, which once made popular mobile phones, have also spiked.

Retail investors on r/wallstreetbets were fiercely critical of institutional short sellers, portraying hedge funds as firms who make money off of exploiting and manipulating markets and media to their advantage. One hedge fund with a particularly aggressive short on GME, Melvin Capital Management, had been the ire of Reddit’s forum dwellers. In one of the top posts on the forum, one Redditor drew parallels with the ‘08 financial crisis, claiming that Melvin was disregarding the law through its “illegal naked short selling” and “obscene market manipulation after hours.” The fund, which is estimated to have lost nearly 30% since the start of 2021 due to the spike, closed out its position in GameStop on Wednesday.

In its blog post justifying the decision to restrict transactions on GameStop (among securities that had been hyped up on r/wallstreetbets, including Nokia, AMC Theatres, and BlackBerry), Robinhood reiterated its mission while contravening it completely. A later update expanded by delving deeper into the mechanics of the decision; from the blog:

The amount required by clearinghouses to cover the settlement period of some securities rose tremendously this week. How much? To put it in perspective, this week alone, our clearinghouse- mandated deposit requirements related to equities increased tenfold. Ant that’s what led us to put temporary buying restrictions in place on a smaller number of securities that the clearinghouses had raised their deposit requirements on.

It was not because we wanted to stop people from buying these stocks. We did this because the required amount we had to deposit with the clearinghouse was so large — with individual volatile securities accounting for hundreds of millions of dollars in deposit requirements — that we had to take steps to limit buying in those volatile securities to ensure we could comfortably meet our requirements.

In deciding to restrict securities, Robinhood needed to strike a balance between its massive liabilities and fiduciary responsibility to its users. The means by which market volatility came about — the Reddit-induced “short squeeze” that resulted in significant profits for individual investors and huge losses for funds like Melvin — went unmentioned. Vlad Tenev, Robinhood’s co-CEO, also denied allegations that the firm’s relationship with Citadel, a financial securities giant to which Robinhood routes over half of its customer orders, had anything to do with the move.

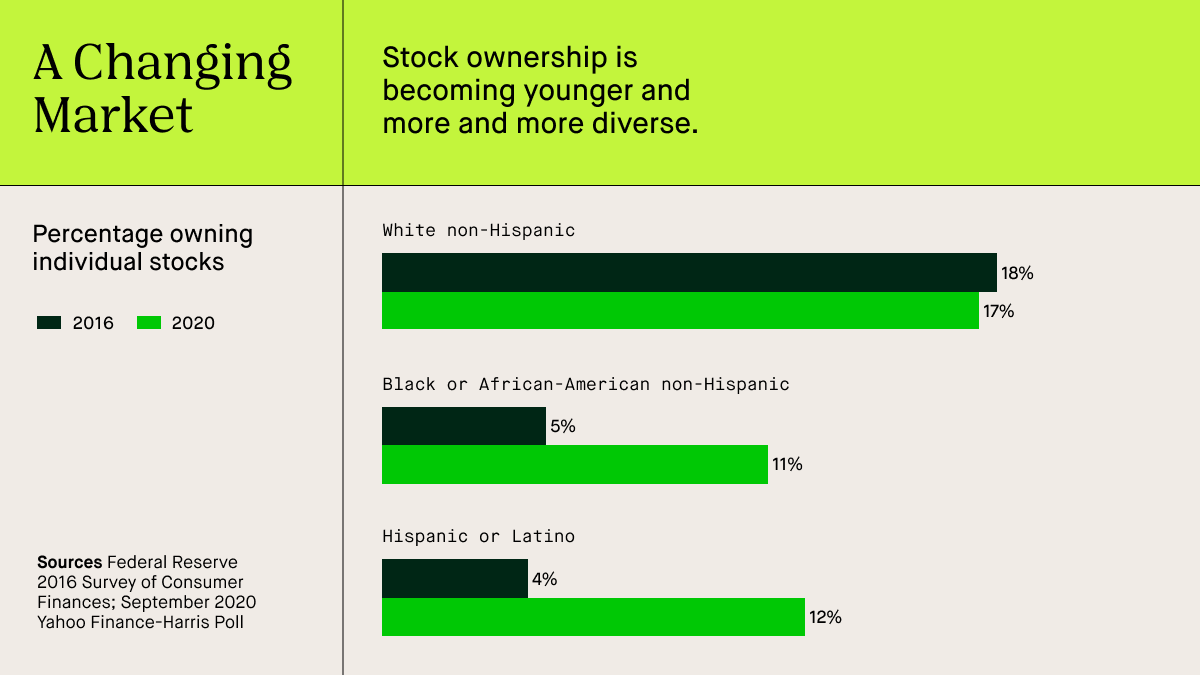

Although other brokers, including Charles Schwab and TD Ameritrade, imposed more moderate restrictions, the public outcry has been so asymmetrically focused on Robinhood because of its purported mission to empower the general public to invest. Baiju Bhatt, Robinhood’s other co-CEO, recently said that “people that previously didn’t feel like the markets were for them are for the first time feeling a sense of inclusivity.” In September, Robinhood posted the chart below on its Twitter to underline their role in driving greater participation in light of the changing landscape in stock ownership.

With the share of stock ownership among African-Americans doubling and Hispanic or Latino tripling since 2016, many new investors have come to platforms like Robinhood which have low barriers to entry. The average user is financially inexperienced, leading the platform to push for improvements in the quality and reach of the financial research it delivers to its users. The app allows anyone to open an account commission-free, forcing other discount brokers to follow in the long run. More than half of Robinhood’s 10 million users opened their first ever brokerage account through the app, and the median age of investors on the platform is 31.

There are a few issues at play. First, the Internet’s transformation of day trading has enabled a greater share of the public to speculate minute-to-minute. In his 1978 book Manias, Panics, and Crashes, economic historian Charles Kindleberger wrote that “at a late stage, speculation tends to detach itself from really valuable objects and turn into delusive ones.” But all trading involves some extent of speculation. Robinhood’s targeted restrictions raise serious questions around the arbitrary mechanics for deliberation.

Another concern is what role brokerages should have in financial literacy. One of the themes in Robinhood’s Thursday blog post was that users were making uninformed decisions, and that “amid significant market volatility, it’s important as ever [to] help customers stay informed.” The decision to restrict trading on a number of securities seems to have originated from a perceived inability to keep the public educated. It’s unclear why Robinhood felt that this particular bout of volatility went over the line. And however well-informed the public becomes, the gamification of trades can quickly offset any educational headway. Features like falling confetti upon completing a transaction or emoji-filled push notifications don’t seem intended to remove the complexity of making investments.

Erik Olin Wright’s definition of democracy is a system in which people “should collectively make decisions over those matters which affect their collective fate.” Robinhood has overlooked the collective consequences its actions have on the general public — not because of its decision to restrict trading on some securities, but due to its continued inability to protect and inform the users on its platform. As it continues touting its mission to democratize finance for all, the likeliest execution of Robinhood’s objective may be the result of external democratic public control over its processes rather than any sort of meaningful internal strategy.